Floor Plan Financing Bonus Depreciation

Kbkg Tax Insight Impact Of Bonus Depreciation For Companies With Floor Plan Financing Kbkg

2019 Bonus Depreciation Update For Auto Dealers Councilor Buchanan Mitchell Cbm

Bonus Depreciation Rules Favor Dealerships With Floor Plan Financing Interest 2019 Articles Resources Cla Cliftonlarsonallen

Product Page Skyline Homes Floor Plans Manufactured Homes Floor Plans Modular Home Plans

Thank You Factory Tour The Home Store Modular Home Floor Plans Two Story House Plans Pole Barn House Plans

2 Storey House Plans Floor Plan With Perspective New Nor Cape House Plans House Plans 2 Storey House Layout Plans

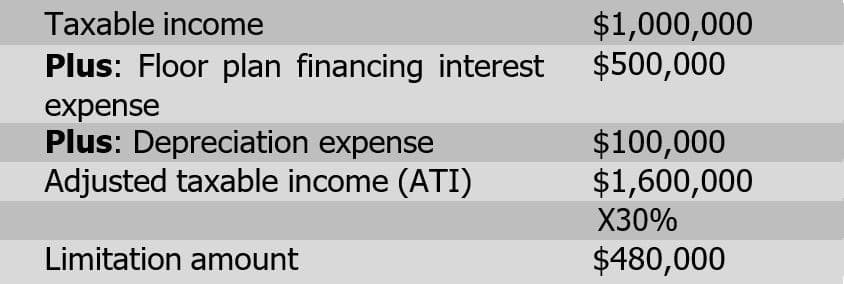

Through some tax planning the automobile dealership decides the new construction location will be owned by a new real estate holding company.

Floor plan financing bonus depreciation.

The Taylor House Plans First Floor Plan Ideas For Kitchen Into Great Room Floor Plans House Plans Garage Plans Detached

Plan 89988ah 3 Bed Craftsman Ranch With Open Concept Floor Plan Floor Plans Ranch Open Concept Floor Plans Ranch House Plans

Cypress Iii Floor Plan Bluestone Eastwood Homes Floor Plans How To Plan Richmond Homes

Plan 33117zr Net Zero Energy Saver House Plan Mediterranean House Plans House Plans Ranch House Plans

Source : pinterest.com